We’re keeping a close eye on the American Health Care Act (AHCA) as it and various iterations of it move around the Hill, and we’ll write more about the impact on early retirees when it’s clear what the fate of it and the Affordable Care Act (ACA/Obamacare/current law) will be. In the meantime, we’re discussing health care and where you might choose to live.

Ranking the States for Retirement

We have all seen those lists a thousand times of the best states to retire to. Florida is a perennial chart-topper for its low taxes and warm weather, and every year some trendy state will enter the mix as the current darling. (This year it’s New Hampshire or South Dakota, depending which list you consult.)

When you make a list that ranks places, you have to make some judgment calls about what people will find important. Not everyone will agree on their most important factors, so the number crunchers can’t please everyone, and I’m not trying to pick on them. But, they tend to focus disproportionately on one factor:

Taxes

Take this 2016 ranking from Forbes, for example, which color codes states entirely by their tax climate:

States with no income tax tend to rank in the top 10 consistently, year after year, almost regardless of what else is going on in that state.

The Weirdness of the Tax Focus Over Other Factors in State Rankings

The logic of focusing on taxes makes sense initially (taxes eat into purchasing power, right?), until you consider that the component of tax that gets the most focus in these rankings — income tax — matters far less to retirees than to those who are employed, because a large share of retirees’ earnings are less-taxed dividends and long-term capital gains, or untaxed Social Security benefits. In addition, states with no income tax like Florida, Texas and Nevada tend to compensate with higher property and sales taxes, which do affect retirees, offsetting the income tax savings.

But the even weirder part of this tax obsession is that retirees don’t actually care that much about taxes, at least relative to other factors about a place. In this Bankrate study, which is the best place ranking I’ve seen yet, they surveyed retirees on what they care most about. The answers:

Taxes are waaaaaay down that list, well behind cost of living and health care quality, as well as quality of life factors like culture and weather. Bankrate did the smart thing and built their list based on what people actually value, and came out with super different rankings than the other currently most cited list, the one done by WalletHub.

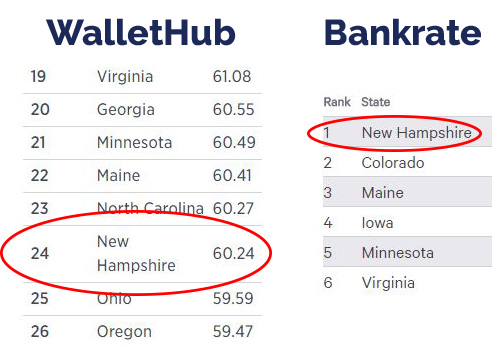

WalletHub’s #1, Florida, is middle of the pack in Bankrate’s ranking, reflecting WalletHub’s tax and warm weather bias:

And vice versa, Bankrate’s #1, New Hampshire, ranked highly for health and well-being (and also taxes) is way down the list for WalletHub:

I did my own informal study, and asked friends on Twitter, in my Slack group, and in real life what they value most in choosing where to retire. Here are those highly unscientific findings:

Full disclosure: “Snow” appearing prominently is from people who want to escape the snow, not frolic in it. Booooo! ;-)

You have to squint a lot to even pick out taxes in that word cloud. Instead, the factors folks mentioned speak very much to quality of life and factors that impact health: the ability to walk and get outside, access to health care, and the ability to engage with friends and family around cultural activities, which is good for mental health.

I suppose it’s possible that people looking at traditional retirement now, late Baby Boomers, are after different things than those of us considering early retirement, mainly Gen Xers and Millennials, but I tend to think those generational stereotypes are overblown, and we’re all not that different from each other. Meaning: some of those rankings are focusing on the wrong stuff entirely.

![]()

Weighting Health More Highly When Considering States

I love that Bankrate gave health more weight than previous rankings did (and to be fair, WalletHub’s ranking, Forbes’ ranking, and others all account for health to some extent), but there’s also a lot they didn’t look at. Which is important because:

Health is the single most important factor for any of us in retirement, whether we think about it or not.

If we are unhealthy, our quality of life is terrible, negating all those other things that might have brought us to a certain place. And if we’re dead, then who cares what our tax rate is?

There are some easy indicators we can look at on health, like life expectancy, obesity rates, smoking rates and physical activity rates that tell us some useful info about states. For example, that the life expectancy by state is almost the exact opposite of the states that Forbes flags as “most favorable” to retirees:

Life expectancy is a complicated measure, and we don’t need to debate the merits of it here, but there’s certainly some correlation between the life expectancy of a state and the healthiness of a state. And, if I may be blunt for a moment, it’s just whack-ass backward to me that anyone would call a state with well-below-average health “most favorable to retirees.”

Here’s the deaths from heart disease map if life expectancy doesn’t do it for you:

No single measure is perfect, nor can it tell the full story, but understanding general health trends in a state tells us a lot about what we could expect to be surrounded by if we retire there. And remember: health is contagious, good or bad. Whether our friends and family are a healthy weight or not correlates to our own weight. Our social circles impact our happiness. And social cohesion in neighborhoods has even been shown to lower rates of stroke.

It’s Not Just Health — It’s Health Care Access and Quality

Note that the people who responded to Bankrate’s study didn’t just respond “healthiness” when saying what’s important to them in a state. They specifically called out health care quality, which is also tied closely to health care access. Because the doctors might be great, but if there aren’t enough of them to go around, or you can’t afford to see them because your health insurance is lousy, then those great doctors don’t do you much good.

We applaud those who include certain factors of health care access in their rankings, for example the Kiplinger ranking that factors in data from a United Health Foundation report that examines supply factors like number of per capita nursing home beds. If you need nursing home care and there are no beds in nursing homes, not many other factors matter.

But this is where that whole health insurance question returns — hence the mention of the ACA and AHCA in the intro — because health care access varies greatly state by state, in large part because of political and policy factors that are rarely talked about when ranking states for retirement suitability.

State Policy and Future Health Care Affordability

Under the current health care law, the Affordable Care Act, states have the option to expand Medicaid, the federal health insurance program designed for the very poorest among us and the occasional child of an early retiree. Under the ACA Medicaid expansion, states can opt to cover families and individuals well above the federal poverty line, which would include many workers in low-wage jobs whose employers don’t offer health insurance. (Those who can’t work are generally already eligible for Medicaid even without the expansion, so the expansion almost entirely benefits people who are working.)

For states that opt in to the expansion, 100 percent of the cost is funded by the federal government, meaning states get to offer health insurance coverage to many more of their uninsured working residents at no cost to the state. After 2020, under the ACA, states have to chip in a little, but the federal government will continue to foot 90 percent of the bill for making health care accessible to wage earners whose jobs don’t provide insurance. Despite what is an obvious federal dollars windfall to states that opt in, not every state has chosen to expand Medicaid. (Put another way, this means states are paying for the expansion anyway through their federal income taxes, but then turning down the thing they are paying for.)

Source: Families USA, April 2017

If the new AHCA bill or some form of it ultimately passes, this particularly bit of policy won’t matter as much, because the AHCA dramatically scales back funding for the Medicaid expansion. But, what does matter about this is what it says about states and their views on providing health care to residents. States generally try to get as many federal dollars as possible, and campaigns ads for Congresspeople and senators frequently brag about how much pork they brought home to their state or district. Not taking the Medicaid expansion when doing so would provide health care to — in some states — well upwards of a million working poor, is a decision driven entirely by politics, especially given the leeway some states have been granted in using Medicaid dollars to fund private health insurance. This isn’t about debating those politics, but rather just noting that they are there and acknowledging the impact they could have on your future access to health care.

Without getting into the politics themselves, I’ll just assert this: It’s worth looking at your current or desired state’s view toward the Medicaid expansion as a proxy for future health care policy decisions.

Those that have expanded Medicaid may be more likely in the future to promote policies that make health care more accessible to more people, perhaps accompanied by a higher tax bill, while those who’ve opted out may take the view that it’s entirely an individual responsibility to provide for one’s own health care. Consider your own preference when making a choice on where to live.

Health Care Costs and Coverage (Could) Vary By State

Another factor to consider when thinking about health care proxies: Pre-ACA, health insurance was partially regulated at the state level — and it could be again.

Prior to the ACA’s passage, states had a tremendous amount of control over what services had to be covered by health insurance plans, and if the ACA goes away, that could once again be true. States could determine whether insurance plans had to cover mental health care services, maternity care and even care for autism. Make sure you know what you’re getting into with regard to a state’s view toward covering key services.

Finally, consider price differences across states. For example, though Medicare is a federal single-payer system, Part D which covers prescription drugs, varies by state in terms of cost and how much it covers.

Source: United Health Foundation

And this Kaiser Family Foundation interactive map provides a detailed look at what health insurance costs in every county in the nation by age and general income parameter — both now under the ACA and under a potential future AHCA. Incredibly helpful for ballparking out what a potential move might mean for your health care costs.

Health Care Access Aside from Health Insurance

Even if we assume everyone can afford to get the health care they need to stay healthy, access in an objective sense also varies greatly by state. Some states simply have more doctors, hospitals and nursing facilities than others. For example, hospital beds per capita vary:

There’s also high variation in number of beds in skilled nursing facilities, number of adults reporting not having a personal doctor, and the number of health professional shortage areas in each state. (And because we can’t truly disaggregate this stuff, it also matters how many people haven’t seen a doctor recently because they can’t afford to.)

Create Your Own Ranking

There’s no perfect state for retirement, and if there was, everyone would move there and drive the prices up, and none of us would be able to afford to live there anyway. Instead, it’s up to each of us to decide what factors we think are important, find the state that best fits that set of priorities, make sure we can live with the downsides of that place, and then forge ahead.

So if you care most about taxes, great. If you care most about being somewhere warm and coastal, awesome. And if you care a lot about your health and your access to affordable health care in the future, then it’s worth looking beyond the rankings to the whole range of other factors that could impact your health and well-being in your early retirement and well into your later years.

Some resources to get you started:

- America’s Health Rankings, with a full report on each state under “explore”

- United Health Foundation’s 2016 senior report, with state-by-state summaries beginning on page 80 (and a lot of this stuff is applicable to non-seniors!)

- Kaiser Family Foundation state health facts

How Do You Weight Health and Health Care?

How do health and health care factor into your decision-making about where to live in retirement? Or do they at all? Are you more swayed by lifestyle factors like how active a place is, or by health and access factors? What do you wish retirement place rankings would prioritize more highly? Any health factors you’re thinking about that aren’t included here? Fire away in the comments!

Source notes: There’s tons of data in this post from the Kaiser Family Foundation, which shares their data freely. They are my go-to resource for anything related to health or health care, and pretty much rock. Thank you, KFF! We are all indebted to you! Non-Kaiser state health factor rankings come from the United Health Foundation’s America’s Health Rankings 2016 Seniors Report, which is amazing in both its detail and readability by non-policy wonks.

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!