This is a post I’ve been excited to write for months, well before we knew where we’d actually land for the year… and now here we are! :::All the shoulder shimmies::: (Bonus points if you want to add in your own jazz hands.)

We’ve been wrestling with a lot of stuff lately, like what the next president means for our health care, whether to use our year-end bonuses to pay off the mortgage or beef up our investments, and what getting ahead of schedule in our savings this year means for our early retirement timing. And today we’ll look at all of that, along with the full fourth quarter chart rundown.

Are you excited? We are!

So much to cover today! It’s a whole year’s worth of build-up. Let’s dive right in!

Our Allocation Decision

I’m super excited to share back on this one! We created our year-end goals in part to guide our decisions of what to do with our bonuses, but we passed our year-end taxable target back in October, well before we got our bonuses, and we only had a manageable bit of the mortgage to pay down to hit our year-end goal.

Now that we know our bonus amounts (which we’re totally happy with though not blown away by, including the little extra that I fought for), we had an even tougher choice to make because of the psychological angle. After bringing the mortgage down to the year-end target we’d set, we still had enough leftover to do one but only one of two very pleasing things:

- Almost entirely pay off the rest of the mortgage, or

- Get the taxable savings and investments up to a very happy and meaningful round number

Originally I was leaning toward mortgage payoff and Mr. ONL was leaning toward investing. (No one was leaning toward the third option: upping our cash reserves.) And somewhere along the way we traded places (noticing a trend?). I just got really excited about the chance to see that particular number on the spreadsheet, which is an unjustifiably dumb reason to make a financial decision, but given two equally good choices, it’s as good a reason as any. But then Mr. ONL said he was game to pay off the house, and I jumped ship like the fair-weather fan I apparently am. (And then I mixed a whole bunch of other metaphors.)

So… we’re (almost) paying off the mortgage!

*Penny would insist that I acknowledge here that that will not make us entirely debt-free, as we still have a mortgage on our rental property that we’re paying off on schedule, not ahead of schedule. But we still think it will feel amazing when we own our home free and clear in a matter of weeks. :::Pretending to be chill about it, but really we’re over here pinching ourselves:::

Where We’re Landing: 2016 Q4 Update

We’re downright stoked with our progress in 2016, despite 2016 being an a-hole of a year in so many other ways. And with blowing past our savings goals and getting the mortgage down to almost zero, it makes the charts extra fun.

If you want to see lots more charts, check out our financial updates from October 2015, the first quarter of 2016, the second quarter of 2016 and the third quarter of 2016. Curious why we don’t share real numbers? Here’s why.

Let’s start with my favorite one first. Is there anything prettier when it comes to mortgage balance than the tiniest possible slice of pie? I’m so proud of us for (almost) paying off our house in less than five and a half years.

And here’s some more context that feels a little mind-blowing, even to us, who’ve been diligently tracking this stuff. A mere 14 months ago, we still owed half of our original mortgage balance, and now we’re down to relative pennies.

Taking a step back, we’ve seen growth in our overall net worth in 2016 that we’re completely happy with, and this is without adjusting upward our supposed property values, which would surely inflate the number even more.

We also see great trends on the year across all of our net worth components… I even had to adjust the scale to make more space for our tax-deferred/401(k) funds.

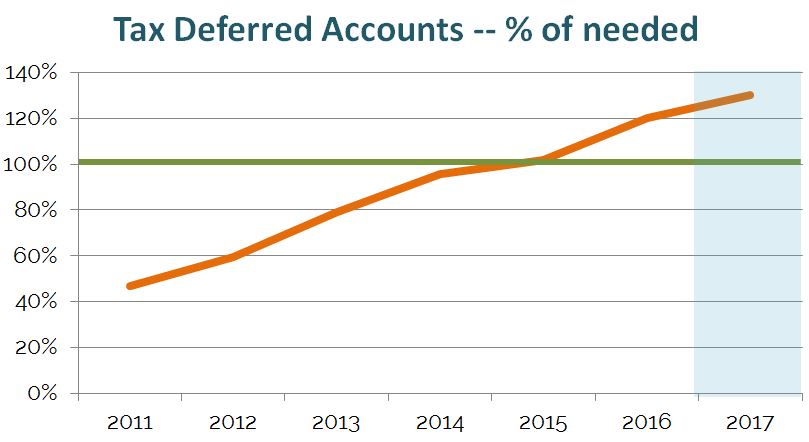

Speaking of 401(k)s, we’re now well beyond what we ever expect to need in those funds, but we still believe in keeping that big nest egg for our later years. We’ll plan to max out again in 2017 for tax reasons and because we can afford to, even though we don’t need to.

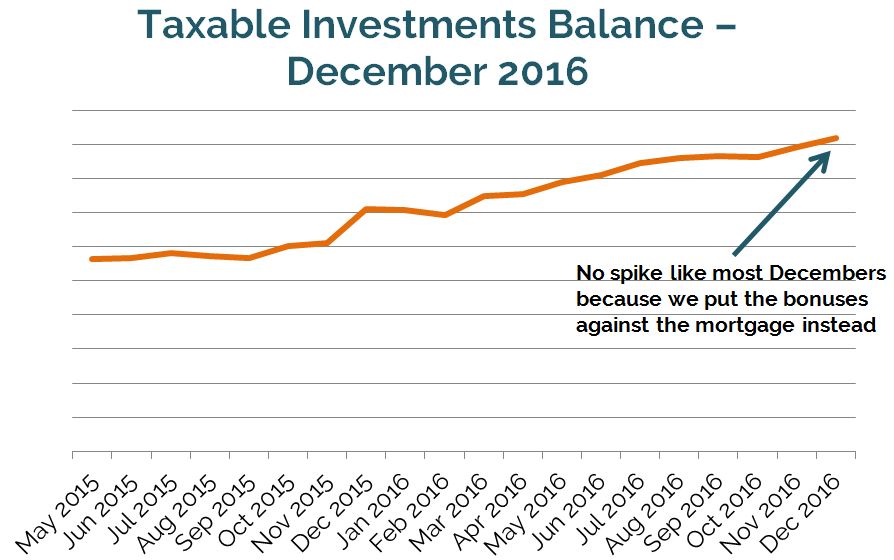

Of course, taxable savings are what really matter to us now, because those funds will support us in the ~18-19 years between when we retire and when we can begin accessing our tax-deferred funds without penalty. And even though we didn’t dump a bunch of money into them at the end of the year this time around, we’re still thrilled with where we’re ending up on the year.

We trended ahead of schedule all year on our taxable savings compared to where we wanted to end up by year’s end, and so didn’t need to dump our bonuses into our taxable accounts to get us where we wanted to be.

Our fast progress this year means that we can officially aim not just for the early retirement number we originally hoped to have, but for our stretch goal, hereafter known as our “magic number.” So from now on our charts will be based on that higher bar:

And finally, where we’re landing on our pie chart showing the percentage of our total goal that we’ve saved in taxable investments each year. We include this chart mainly so that anyone who’s curious can see how fast it’s possible to save up for early retirement. We’re slightly shocked that we still hit this big a chunk of what we need to save this year, given that we almost paid off our house, too. This is based on our lower original ER number, not our magic number, so we’ll have to represent this differently in our quarterly updates in 2017.

There you have it on the charts. That’s where we are at this point in time, and now we look ahead to what it all means for when we can pull the ripcord!

—> Follow along with our adventures between blog posts — all the non-financial stuff! — on Twitter, Instagram and Facebook. <—

The Timing Question

The last few weeks have been a good and important reminder to us that you can never over-communicate when it comes to money. We thought we’ve been having the same conversation, but turns out we were actually having two different ones. When I was talking about quitting earlier than end of next year, it was under the assumption that we’d hit our stretch goal early — and when Mr. ONL was talking about working til end of 2017, it was under the assumption that we wouldn’t hit our number until year end. So he heard me saying I wanted to quit before we’d hit our number, and I heard him saying that we had to finish out the year no matter what… and neither was what we were actually saying. SO… turns out our difference of opinion was actually a sameness of opinion, just expressed differently.

But the great news is that we have been on the same page all along, and just didn’t realize it. (More evidence that burnout is bad for marriages — it limits time to discuss this stuff in detail!) And that makes our decision on early retirement timing easy. Here’s our plan:

Work until one of the following two things happens:

- We reach the end of 2017, or

- We hit our stretch goal in our taxable savings and investments (our “magic number”)

Technically we’d also call it quits if one or both of us gets laid off, but we’re not pursuing that. So whichever ball gets to the end of the funnel first gives us our exit!

That will trigger our giving notice and seeing if those prorated bonuses are more than a rumor (though we won’t count on getting one more penny after we give notice — anything extra at that point will be gravy). Given that we’ll be saving faster in 2017 than we could in 2016 (see below!), we should be to our magic number no later than October, but it could come faster with market help… or come slower with market headwinds. But our plan is the same either way, and we’re as committed as ever to leaving at the end of 2017 even if we’re not at our number.

Financial Plan for 2017

In addition to the goals we’ve already shared for the new year, here are our financial to do’s, based on where we’re landing and our revised timing plan:

Pay off the last bit of mortgage on our home — We’re coming close to pay-off this year end, but will have a small lingering balance that we’ll knock out in February or maybe even January. We’ll share the big “Ding dong the mortgage is dead!” announcement when it’s time!

Amp up our monthly investing like crazy — As soon as the mortgage is gone, we’ll be able to redirect that money into investments/savings each month, which will accelerate our pace. With the small raises we got added to the money we no longer need for the mortgage, we should be able to increase our monthly investing by 50 percent.

Hit that magic number as soon as we can — Though we’re huge believers in pacing yourself and making sure that you still enjoy your life en route to early retirement, being so close, it will be awfully tempting to just hurry up and get to our magic number. Because impatience.

Take care of health care ASAP — We said in our pre-retirement to do list post that we’re going to go health care nuts in our final year of work, but now we’re moving up that timeline, just in cases (#loveactually). We see our primary docs right at the start of January, and then we’ll be in for a whole bunch of specialist visits, just to make sure we check out everything worth checking out. Then we can go into early retirement with a thoroughly clean bill of health, which should provide some peace of mind in case the future of health insurance is unclear at that point.

Aim higher on charitable giving — We felt happy to devote a bigger share of our income to charitable giving this year than we have in the past, and we want to continue that in 2017. We’re going to look into setting up a donor advised fund before we pull the plug so we can do some sustained giving even in our lower income years.

It’s a lot to do, but we’re motivated like crazy to make it all happen, and fast. Thanks for coming along for the ride!

Our Best Holiday Wishes to You!

It’s been pretty amazing to hear from so many of you guys with well wishes for our bonuses and our early retirement timeline. It feels downright spectacular to feel you rooting for us virtually. And we hope you all know the feeling is mutual. We’re rooting for all of you whose plans we know, and for those who’ve never dropped a line, it’s not too late… we’d love to send some good FIRE vibes your way. But regardless of whether you want to share your journey, we’re sending out lots of holiday love to all of you. Your support means so much to us, and makes this path to early retirement a thousand times more fun.

*** HAPPY HOLIDAYS! ***

I’ve been writing a lot lately about feeling burned out at work, and so I’m going to take the full holiday period off to relax and enjoy deadline-free time with family and friends. Back at ya January 2nd! xoxoxo

Let’s Discuss!

How was your 2016 in total? Any new or big goals for 2017? Anything you’ve recently realized or decided? For aspiring early retirees, how’s your timeline looking? Anything we can give you a virtual high five for? Let’s chat!

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!