Overheard in the ONL house:

Me: “What should we do with our allocations this month? All to Vanguard, or start focusing more on the cash cushion?”

Mr. ONL: “It’s really hard not to try to time the markets right now. But we also said that a year ago, and we’re up more than 10 percent since then.”

Me: “I know, but the last quarter has just been ridiculous. I don’t believe it will stick.”

Mr. ONL: “Yeah. Can we get a correction soon, please?”

That’s the conversation we just had, as we think about where to put the non-automated part of our April savings and investments. And I can definitively say this, at least for us:

Getting close to early retirement comes with a whole slew of conflicting emotions.

Excitement at how close we’re getting. It’s haaaapppppennnnning. Trepidation at the current state of the markets, and the possibility that we could be facing a crash or recession in the early part of our retirement, which is the biggest predictor of savings not lasting (sequence of returns risk and all). Thrill at knowing that the next time the snow starts dumping, we’ll be retired, and can ski midweek. Impatience to get to all the cool projects we have planned for our post-career lives. Nostalgia for all the career things we’re doing for the last time.

So far 2017 is flying by. I can’t believe I’ve already flown 36,000 miles and stayed almost 40 hotel nights. I definitely can’t believe that our investments are up almost 8 percent in just the last quarter (including our contributions).

United activity for the quarter

This time-flying feeling should be a good thing, right? How amazing to get to breeze through our last year of work quickly (not that the work part is actually a breeze — it’s still work!).

The super weird thing — one of those conflicting emotions — is that I’m actually wishing the year would slow down a bit. As it’s dawned on me that many of the work things I’m doing are happening for the last time, I’ve started to wish that I could stretch some of them out. Especially time with work friends, time with clients I love, time in places that work takes me, time doing my favorite stuff like presenting, and — not gonna lie — time in first class (free upgrades, of course — I would never charge clients for first class) and in nicer hotel rooms than we’ll ever pay for ourselves (Residence Inn, here we come!).

The huge upside of this nostalgic impulse is that it helps me keep the frustrating moments in perspective: “Awww, frustrating coworker. You’re doing that annoying thing that used to make me crazy. But now I’m thinking about what a great laugh I’ll get when I look back on how important you thought this was, when it really doesn’t matter. Bless your heart.”

Of course, at the same time that I’m feeling all of that, there is still some part of my brain that doesn’t believe this early retirement thing is really happening. I’m still completely invested in long-term planning discussions at work, when I could easily sit back and feel smug in my secret knowledge. I still talk to clients as though we’ll be working together for years, because of course they’ll still work with my company, just not with me. And I’m still trying to keep my revenue and billable hours high, as though those things still matter (they don’t). (I’m still doing pretty well at saying no to things I don’t want to do, though, and I’m not working long hours when I don’t need to.) And, yeah, those numbers feel as big and fake as ever.

So that’s the backdrop for what’s going on with us right now. And it’s the lens through which we’re looking at our finances, and assessing the bonkers market growth of the last quarter. Let’s get into the update!

The Time for Countdowns

We’ve been watching the months tick down on our little sidebar counter for more than two years now, and it currently stands at 9 months:

But we realized, that countdown is less meaningful than the countdown to when we give notice, because our work will lessen dramatically after we tell people we’re leaving. And while we’re still not settled on some key questions like whether we’ll give notice at the same time (more on this in a post soon!), or exactly when we’ll each do it, we do know that the latest we’d possibly give notice is mid- to late-October, meaning our real ticker is actually:

And when we’re thinking about countdowns, it’s impossible not to think at the same time about the countdown to when we can unmask ourselves here, and stop this anonymous silliness. We expect that to happen not long after we give notice at work, so sometime less than seven months from now, we hope before FinCon at the end of October. (We can actually be in pictures this year!) Meaning our full countdown currently stands at:

Countdown to giving notice: 6ish months

Countdown to no-more-anonymous-blog: < 7 months

Countdown to the end of work: < 9 months

That six months number especially is soooo sooooooon. Someone please pinch me. Is this real life?

—> Follow along with our adventures between blog posts — with so many more pictures! — on Twitter, Instagram and Facebook. <—

The Financial Update

Part of me wants to put an asterisk on all of these charts, like the asterisk on Barry Bonds’ record-setting home run season. Because, for real, are these gains going to stick? You’re welcome to give us the pep talk on not timing the markets, and how time in the markets is the most important thing, though of course we know all of that.

Knowing it rationally and feeling it emotionally are two different things.

We’re still staying the course on our investments, with a little more shift into cash with the money we’re no longer paying against our primary mortgage. But we’re not attaching ourselves to the current positions, which is a good practice no matter what the markets are doing. And we’re not assuming that we’re as close to our magic number as our current positions suggest. So with that, here we go.

(As always, we share relative numbers and percentages only. Here’s why. And, all of the axis units are not obvious numbers and many of the charts don’t begin at zero. Just to be tricky like that.)

Property and Debt

We paid off our house in January of this year, so this chart won’t appear in future quarterly updates. We went from owing about half of the original mortgage balance in October 2015 to having it fully paid off 15 months later:

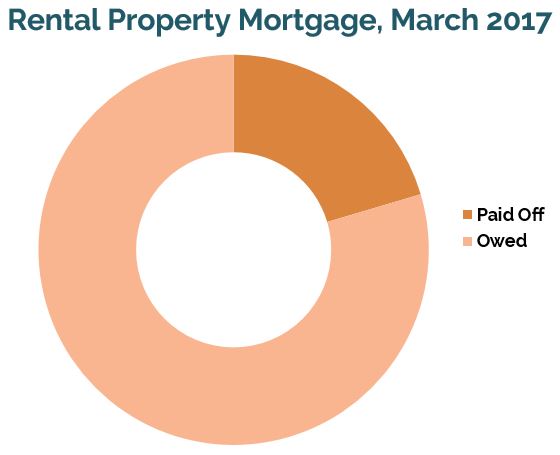

And our most boring chart, what we still owe on our rental property mortgage, which we are not paying off ahead of schedule (here’s why not):

Taxable Savings

Now that the house is paid off, taxable savings is by far the most important element of our two-phase retirement plan, given that our 401(k) balances are now high enough that we could lose 30 percent of their value, never recover it, collect conservative annual gains from the remainder, and still double our spending when Mr. ONL turns 59 1/2. Compound interest is magic.

Taxable savings is what we base our target number on, and it’s what we’re most focused on in this final year of work, including both our invested assets that aren’t tax-advantaged, and the two-year cash cushion that we plan to have before we quit.

Because some of you have asked, here’s what our current taxable funds allocation looks like, before we’ve built up the full two-year cash cushion we plan to retire with:

And after the asterisk-inducing first quarter of 2017, here’s where our taxable savings stand:

That puts us well in range of where we should be at this point in the year to hit our target, and possibly quite ahead considering that a large chunk of our income will come at year-end, what we’ve taken to call our “retirement thank you bonuses.” (Mine will be teensy, but Mr. ONL’s should be decent-sized.) But again, we’re thinking of this number having a big asterisk on it, so we don’t assume we’ll be continually going up from here.

Net Worth Components

As for total net worth, which doesn’t include depreciating assets like cars and is built on property value assumptions that are extremely conservative, here’s where things stand. To us, that’s a looney bin bump since the end of 2016.

And on the components, the big dip on mortgages reflects the home payoff, and the 401(k) line is where you see that big market increase that feels an awful lot like a bubble to us.

You can see that clearly here, in our 401(k) balance tracker. At the end of Q1, we’re already where we’d expected those balances to be sitting at the end of the year, including two more matches we haven’t yet received.

New Addition: Travel Points

Given that travel miles are an important part of our portfolio, we’re going to start including them in our quarterly update. So we are sharing some numbers after all!

And while it looks itty bitty by comparison, the notable thing about the Ultimate Rewards column on the right is that I only signed up for that card in mid-January, right before the online 100,000 point bonus expired. That’s what happens when you travel a lot for work, and the card offers 3x points on travel. (We haven’t decided if we’ll keep the card past this year, but we are not sad about having those UR points, especially for when we don’t want to fly United.)

– – – – – –

So will the numbers stick? Is a correction coming our way? Your guess is as good as ours! But man, we’d sure rather if that correction comes this year instead of next, if one is coming at all.

How was your first quarter?

I’m guessing that nearly everyone had a pretty great first quarter in the markets, but any surprises for you? Any predictions you’d care to share for what the markets will be doing in the near future? Any successes we can help you celebrate? Let’s discuss it all in the comments!

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!