A hot topic around here lately has been the question of whether early retirees in the U.S. should count on Social Security in their calculations for their 60s and beyond, particularly as I’ve tried my hardest to make the case for a more conservative approach both to projecting what we’ll need and to the amount we save in the first place.

In our case, we are not banking on Social Security payments coming our way in our 60s, which isn’t to say that’s the best plan or the right plan — it’s just what feels right to us. (It’s also possible for us, which is a different thing, and something we’ll discuss.) Let’s dig into all the issues here, and then let us know in the comments how you’re thinking about Social Security.

This is part 2 in a mini-series on Social Security and Medicare, two under-discussed topics in the early retirement community. Read the first part, on the dangers of planning for level spending over time, here.

As always, my goal in writing about this isn’t to profess to know all the answers, it’s simply to ask more questions that might help strengthen a plan you’re working toward. So our choice not to build Social Security into our plan might still help you think through the details on how you would count it in yours.

Why We Aren’t Banking on Social Security

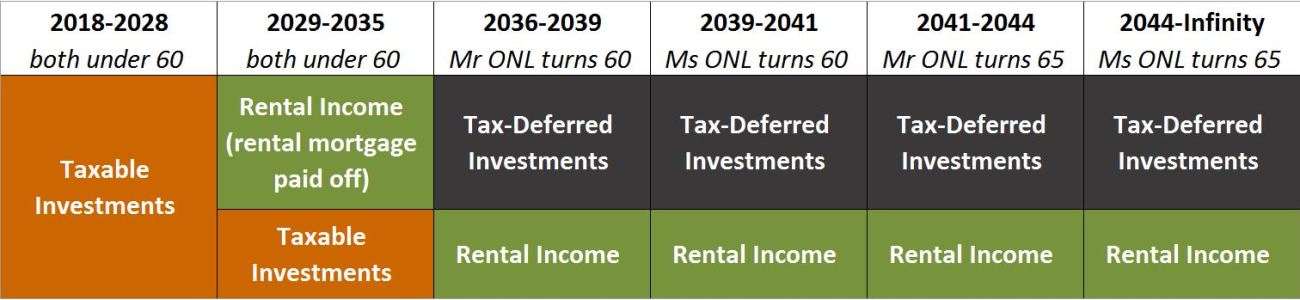

As a reminder, here’s what our phased out retirement income plan looks like, not counting any passion project work we might take on:

Because we’ll have multiple income sources in our post-60 years that we consider reliable (rental income is our way of diversifying so we’re not wholly market-reliant, and our 401(k)s only need waaay-below-historical-average gains to support us at a higher level when we hit 60), we’re in the fortunate position of not needing to count Social Security, and we know we’re lucky to get to say that. It’s certainly not true for everyone. But there are several other big reasons we don’t count Social Security in our projections, even though we expect it to be there for us at some level.

Here are those reasons:

The benefits will change, which is hard to plan around — Though analyses differ on how much longer the Social Security trust fund will stay solvent without policy intervention, the fact remains that Congress will be forced to reform Social Security at some point in the not-too-distant future. There are a range of ways they could ensure that the program has enough money coming in to pay for the benefits going out, from removing the cap at which individuals’ pay has Social Security (FICA) contributions taken out of it, to raising the full retirement age again, to creating a sliding scale that provides larger benefits for lower income people and smaller benefits for higher income people. I suspect the age shift will not be a popular solution because the average retirement age (62) hasn’t gone up in years, despite Social Security’s full retirement age moving to 67, mainly because the majority of people don’t retire by choice. The other two options hit higher income people in particular, which always becomes extra touchy on a policy level. So there won’t be an easy answer on this, but until there’s an actual long-term fix in place, it’s wise not to bank on getting as much as the calculators may say you’re entitled to.

The benefits could even disappear for high net worth people — Though Congress has not recently shown any hunger for implementing means testing on affluent people, most of us in the early retirement community are looking at long timelines, over which just about anything can happen. (Consider: nine years ago, California voted against same-sex marriage. California! And now it’s legal everywhere. That was a difference of only a few years.) And it’s not unthinkable that Social Security could be reformed in such a way that everyone pays in, but only those who truly need it get the benefit, meaning those of us with high net worth or other large income streams may no longer qualify. Medicare is already partially means-tested, and whenever Medicare comes up, there’s always talk of adding more tests or making premiums more closely tied to income. There’s no reason Social Security couldn’t adopt some of this same logic. I don’t believe it’s likely that some higher net worth people will lose the benefit altogether, but stranger things have happened.

Social Security has tended not to keep pace with real inflation — As I shared in part 1, the cost of living adjustments (COLAs) built into Social Security are pegged to the consumer price index (CPI), which is not considered to be a good measure of actual expenditures for seniors. Meaning Social Security payouts lose real spending power every year, making it a little like counting on a depreciating asset to hold its value. While there’s no reason to think that Social Security benefits will fall totally out of step with real-world costs, but there’s also no reason to think they’ll ever start keeping up with real price inflation.

We love contingencies, and Social Security is good gravy — If you made me choose between A.) saving an amount that felt comfortable and coming to realize in hindsight that we’d saved too much and worked too long, or B.) saving an amount that felt mostly comfortable but allowed an earlier escape from work and coming to realize in hindsight that we’d saved too little, I’d choose A every single time. Trading a year or two of work for decades of financial stress or worry? To me that’s a dumb trade. I’d rather work another year or two and be free of that anxiety. Which explains why we have saved more than lots of folks would say we need for the lifestyle we plan to live (though we don’t think we’ve “oversaved” — we think too many people undersave), and why we have a whole slew of contingency plans. And we think of Social Security in that same category, as something we might be able to fall back on if our original plan fails, but which we aren’t banking on. And if our phase 2 retirement happens to get graced by some extra income? Well great. Maybe we’ll fly first class once in a while. (Or, more likely, we’ll ramp up our charitable giving.)

We’re happier with one less moving target in our lives — We already have the biggest source of uncertainty (health care) to worry about, and that’s plenty. The markets come with their own uncertainty. Given that we don’t need Social Security, we’re happier just not even thinking about it, because it’s one of those things that can bring on a headache awfully quickly once you dig deeply into it. (Especially after you see that there are at least four different benefits calculators at various places on the Social Security site. All of which may give different answers, depending on the day of the week. I am not exaggerating.) So while that may seem like a silly reason, I’ll fight anyone who tries to argue that there’s no value in doing things for happiness reasons. (That’s completely why we paid off the house, and that has paid HUGE happiness dividends. Which is worth quite a lot of money to us.)

It’s simply possible for us to ignore Social Security — We are in the fortunate position of having saved early and often in our tax-advantaged accounts, and of also having had the means to keep maxing those out while also saving a lot in taxable funds. It’s why we don’t have to sell out our future selves by relying on backdoor Roth conversions to fund our early retirement, and can instead leave that money alone to grow so that it supports us in comfort in our 60s, 70s, 80s, 90s and 100s (I’m optimistic like that). We know not everyone can do that, and I’m not about to tell everyone who can’t that you better plan to work forever, then. But if your plan does lean heavily on backdoor Roth conversions to work, it’s worth considering whether you’re also leaning heavily on assumptions of level spending over time, and I’d argue you should plan to step up your spending every few years because of expenses like health care that significantly outpace inflation.

Considerations If You Are Counting on Social Security

The older you are now, the less likely any changes to the program will affect you. If you’re 55 now, you can probably use the Social Security calculators out there to get a pretty good idea of what will be coming your way in a few years. But if you’re 25, different story. Wherever you are in your journey, if you need Social Security to make your plan work, here are some considerations:

Know how benefits are calculated — You only qualify for Social Security if you’ve earned income in at least 40 quarters (10 years), and your benefit entitlement is calculated on the average of your top 35 earning years, indexed into today’s dollars. And many early retirees are willingly putting a lot of $0 income or small numbers into that average. (Only earned income counts, not things like dividends and capital gains.) If you earn $100,000 for 15 years, but then have 20 $0 years, your average is only $43,000, which puts you well below the maximum benefit. Right now, that would get you a monthly benefit of about $1200. As opposed to if your average was $100,000 over those 35 years, which would get you $2100 a month. (These are rough estimates — the actual calculation formulas are complex and have multiple variables.) Of course, in reality, even those of us who are high earners now have plenty of entry-level or just above entry-level years included in our average, so the actual benefits you receive as an early retiree could be quite small.

Consider the benefit of delaying — Social Security now considers full retirement age to be 67 for those born after 1954 (66 for those born ’43-’54), while previously you could get your full benefits at age 65. We should all expect, as reforms happen, that there will continue to be incentives built in to entice us to wait until we are older to claim our benefits. Right now, benefit amounts increase 8 percent for each year you delay the start of your benefits, up to age 70. But that could go even higher. So the later you can wait to claim Social Security, the better in terms of the total dollars you’ll receive if you live for several years beyond when you claim.

Keep projections extremely modest — Knowing that Social Security doesn’t always keep pace with inflation and that some program changes will happen out of necessity, it’s wise to base your projections less on what they might look like today, and more like what they could look like with some major downgrades. I’ve heard some readers say they anticipate getting 25% less than they’d get today and others say they project as much as 50% lower. As with everything, it’s your call what projection will let you sleep at night!

This Motley Fool article has the best simple breakdown of how Social Security amounts are calculated currently (it’s a complicated formula), and what the amounts are this year. I highly recommend it!

How Are You Thinking About Social Security?

Where’s your head in all of this? Are you banking on Social Security? Why or why not? Do you aim low on what you’ll receive if you do count on it? How did you decide what to project? Please share allllll your thoughts in the comments, and let’s discuss!

And I specifically wrote this article to U.S. audiences, but if folks from other countries have read this far, please share with us how you’re thinking about your own country’s retirement benefit. Many of the countries with the strongest safety nets (i.e. socialism) also have the largest looming demographic crises, with low birth rates and high numbers of impending retirees, meaning the systems may not be able to bear the cost of government pensions for all. Lay your non-U.S. insights on us!

P.S. HUGE THANKS to everyone who nominated Our Next Life for the Plutus Awards. ONL is a finalist for the second year in a row for best Early Retirement/FI blog, aaaaaaand ONL is one of ten finalists for Blog of the Freaking Year. (“Freaking” added by me for emphasis, to reflect my enthusiasm level.) I feel like it’s raining gold stars, you guys. You rock. (FinCon also called ONL out as one of five breakout blogs this year, along with some other friends! How cool is that?) Oh yeah, and I’m quitting my career today! A lot tucked into this P.S., eh? ;-)

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!