I love the financial independence/early retirement blogging community fiercely, and I’m proud to be a part of what is unquestionably one of the most positive, supportive places on the Internet. I didn’t even really read FI blogs before we got started on our journey, or before I started blogging for that matter, but I’ve still gotten so much from them, and from the community of readers who comment and share thoughts, too.

For those of us interested in living a particular kind of unconventional life made possible by the subtraction of work, FI blogs serve a crucial purpose.

And that crucial purpose is why it’s so critical that we always tell the full story.

Last year, I wrote my feistiest post to date (possibly ever – depends how this one goes!), in which I encouraged readers not to listen to FI blogs, especially when it comes to the question of whether early retirement is sustainable, because too often they don’t tell that full story. (Bottom line: nearly every retired FI blogger draws significant income from their blog, and therefore isn’t actually testing the approach to early retirement that they espouse.)

That post started some great discussions, and I was pleased to see a few more bloggers disclose their blog income as a result. But that alone isn’t enough.

So today, I’m going farther. This is a manifesto of what FIRE bloggers owe our readers. We’re at our best as a community when we push each other to be better, and this is my big nudge to all of us, including to myself.

The predicament I see with FI blogs is, interestingly, that many are too encouraging. This may be the one and only time I ever complain about a group of people being too positive, but the fundamental conflict is that if we make early retirement seem too easy to achieve, or too simple mathematically, we lead folks down the primrose path to potential financial ruin later in life, at exactly the time when they are least equipped to deal with it, because they simply did not save enough to weather all the future unknowns that none of us can control. We need to be both encouraging and realistic, and sometimes full realism is what’s missing.

Problem One: The Plan Vs. Reality Mismatch and the Incomplete Message That Creates

Let me make this completely clear: I do not think that making money from your blog is the problem here. I know how much work it is to write a blog and keep it going, and I believe people deserve to be compensated for their work. So if you make money on your blog? Great job!

The problem is that what folks espouse and then what they actually do are often quite different, and that creates a real and important issue in the message. Let’s break that down.

Consider the most commonly discussed levels of financial independence or early retirement:

While bloggers may have different approaches to getting to financial independence, the model of post-career life that most espouse is this one:

No inherent problem there! Never having to work ever again is what we all want in an ideal world, right?

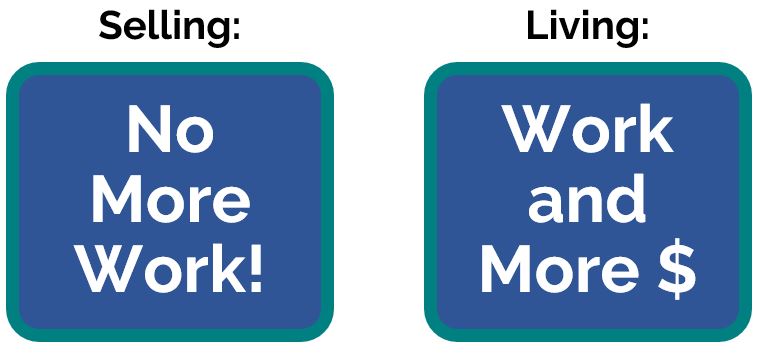

Here’s the problem:

Or, to put it more simply:

It’s understandable if you spend all these years working a high-stress job, thinking you never want to work again, and then get to retirement and realize that there actually are certain types of work that you wouldn’t mind doing. (Hi. We did that.) Or your blog grows because you achieve financial independence and become a big inspiration to people and realize that you can make big bucks from that. All well and good.

But imagine this scenario:

A blogger who needs retirement cash flow of $40,000 a year saves a million dollars and leaves their career. Great! They quickly begin netting $50,000 a year from their blog, and now instead of withdrawing $40,000 a year from their portfolio, and actually testing the 4 percent rule they espouse in their posts, they are now not withdrawing anything, and are instead reinvesting dividends and even adding $10,000 more to their portfolio on top of market gains. In no time, their portfolio balance hits $1.1 million, and then $1.2 million and beyond. Should the blogger’s blog income ever disappear and force them to default back to their original withdrawal plan, they’ll now only be withdrawing 3.3% of their portfolio each year, not 4%. If the economy tanks, they can sustain a 17% correction before they’re even back at their base level they need to be completely financially independent forever. Or maybe they have a $200,000 cushion on top of their FI fund to weather things like higher future health care expenses or a home purchase if they decide to move somewhere higher cost.

The question is: If this person keeps blogging about the likelihood that the 4 percent rule will be adequately conservative in the future, or whether an economic crisis would sink their finances, or about why “enough” is a lot less than you think and you should stop working already, or whether we should all be more confident about our early retirement money working out just fine, should we trust that?

There is an unstated social contract at play in the FIRE blogosphere between writer and reader which says: You can trust what I’m telling you and incorporate my ideas safely into your own retirement plan because I’m actually doing this myself and betting my own finances on it.

Of course it’s still the reader’s job to consider the source and do your own homework, but when bloggers break that contract, the least they can do is tell you.

Problem Two: Ignoring the Reality for Many Readers

I appreciate the lengths that so many bloggers go to to make readers of all stripes feel welcome here. It’s why I write posts like how I started with essentially nothing saved only 10 years before retiring early. And I’ve heard from enough readers to know that that inclusive spirit is absolutely a positive thing.

But there’s a dark side to that: To be inclusive, we often have to act as though the things we say apply to everyone, and that’s just not true. Looking at income breakdowns in the U.S., for example, most people simply cannot save for early retirement in 10 or 15 years without spending so little that it’s below the poverty level, an impossible reality in the age of housing shortages, massive student debt, skyrocketing health care costs and wage stagnation. Sure, some people can save in that time frame or more quickly, but they are not the norm.

So when we say “anyone can do this,” or start throwing out big numbers or percentages that are clearly out of the mathematical realm of possibility for the majority of people in one of the wealthiest countries on Earth, we’re actually excluding with our attempts to be inclusive or, worse, we’re shaming those who can’t save at those levels for being less capable or dedicated.

I don’t believe that the answer is to be less inclusive, but simply to acknowledge a much wider range of economic realities. And if you aren’t sure what those realities are, keep reading.

I think we as a community of FI bloggers are already doing a great job on the encouragement side, and that won’t change, nor should it! So the encouragement part isn’t represented here in the manifesto. Where we’re lacking is on the realism side, both our own as bloggers, and potential future problems readers could face. And that’s where we can and must do better collectively. That’s true for both the big, influential blogs, and the small blogs, too, because they could be the influential blogs tomorrow.

The Manifesto: What FIRE Bloggers Owe Our Readers

Be Transparent About Whether You’re Testing Your Own Plans – If we write about the 4% rule and taking an approach to saving that embraces more risk, then we need to be living by the 4% rule and not continuing to pad our investments. Or if we find ourselves unexpectedly making good money in retirement (good for you!), we need to be clear with readers that our plan has changed and we’re no longer doing what we said we’d do with respect to our finances.

Share the Parameters of Your Own Financial Independence – Not all financial independence is created equal. To one person, financial independence might mean that if you never work again, you won’t be comfortable but you won’t starve, while to someone else, FI might mean being able to live large forever. Readers deserve to know what standard of living is build into your definition of financial independence, whether it covers only you or you plus a spouse or family, whether it relies on living in a particular place like a low cost of living area or overseas, and whether you’re factoring some future work into your numbers or not.

Acknowledge If You Have a High Income – I get that “high income” means something different to everyone, and that if your income matches those around you it’s not going to “feel”’ high. But I see way too many bloggers saying “Anyone can do this!” or characterizing their own situation as normal, average or the massively misused term “middle class” when it’s clearly not, and that both misrepresents the truth and alienates readers who can see through it. But let’s take the ambiguity away from what “high income” means. Here are some facts: the 50th percentile of household income in the U.S., per 2014 Census data, is $57,000 per year. That’s with an average of 1.41 earners, meaning the individual average is just above $40,000 a year. So if your household earns above these figures, you already earn more than average. If your household earns above $80,000 a year you’re in the top third of all households, above $100,000 you’re in the top quarter, $160,000 puts you in the top 10 percent, $200,000 is top five percent and $250,000+ is top three percent. That’s household, not just one person in a dual-income home. Even earning top quarter ($100K+ for the household) puts you well above average and about double what most households earn, so is going to materially impact what you’re able to do financially and the rate at which you can save and invest. That’s why you must say so. (It also means if you earn six figures as a household, you’re – by the most generous possible definition of middle class as the middle half of everyone – not middle class. To say you are is untrue.) And if you’re in the top ten percent or higher, then you absolutely need to clarify that what you’re doing is going to be out of reach for the vast majority of folks. I’ve always acknowledged that we earned well above average, but I can do better and owe readers that. Our lightning fast saving for early retirement was absolutely aided by having a household income in our final saving years that was in the top three percent, along with not having kids. It wasn’t always there, of course, but when it was in lower brackets, we saved more slowly.

Tell Readers If You’re Working – This one doesn’t need elaboration, but it’s important for readers to know if you’re still drawing an active income. And as two people who telecommuted for years, I can absolutely affirm that just because you’re doing it from home, it doesn’t mean it’s not “real work.” If you left the office but are otherwise doing your job, it’s still work.

Be Clear About the Limits of Good Intentions – We can talk all day about how important it is to be flexible, but how flexible can you be if you’re 75, you haven’t worked in three decades, the cost of Medicare has tripled so that health care is now your largest expense, and you just found out you have stage 3 cancer? Is that when you’re going to “just go back to work”? Of course we all must stay on top of our spending in early retirement (and traditional retirement), and constrain it if the markets start tanking. But we owe it to readers to remind them that flexibility and frugality have their limits, and sometimes the only answer is to save a bit more or build in more contingencies.

Drop the Health Arrogance and Ableist Bias – This is going to sound harsh, but many bloggers are either blind to this or are deliberately choosing to see themselves as better than others simply because they are currently healthy. And hey, lucky you. There is a lot we can all do to improve our chances of staying healthy over the long run, and if you aren’t focused on staying active and eating healthily, I think you’re doing it wrong. But to say to your blog readers that you can control the costs of health by making healthy choices is straight up lying to them. First, none of us can control the cost of health care, and health insurance alone is currently going up in many states by 20 percent a year. (That’s about seven times the rate of overall inflation, each year.) And that’s before the expected cuts to Medicare arrive, even though the average Medicare recipient already has to pay more than a quarter million dollars out of pocket on health care between when they get on Medicare and the end of life. But more importantly, anyone can get sick anytime. Even the healthiest people. Or you could get hit by a car and need massively expensive surgeries and hospitalization. We can and should do everything we can to improve our odds, but we can’t even begin to control this stuff. Because health isn’t something you can plug into a spreadsheet. So don’t talk about it like it is.

Talk About Your Backup Plans and Their Limits – If your plan fails, what happens? Do you have contingency plans you can fall back on, like a home you own that you could downsize to free up resources? Do you have family you could move in with if it came to that? Do you have family connections that would let you move to another country with free or inexpensive health care? All of this stuff matters, because it provides your reader with important context. Saying it’s fine to save slightly less than your numbers suggest you should means something different if it comes from a blogger who has a big fat safety net versus one who doesn’t, and readers deserve to know your context to assess whether your advice feels right to them.

Consider the Usefulness of Partial Numbers – There’s no need to share your actual numbers if you’re honest with readers about your general financial situation, particularly on questions like whether you have or had student debt, the range of what you earn(ed) and whether you’ve had any windfalls that have sped your progress. But if you don’t share all of your numbers, consider whether it’s useful to share any of them. A popular metric to share is savings percentage, and there was a time when I shared ours too, but if you don’t specify the “Of what?” answer, the percentage itself will shame some of your readers into feeling that what they’re saving is a fail, and it will tell others that you must have such a crazy high income to save that percentage, and therefore you can’t possibly be talking to them. Better metrics to share are those that could truly apply to anyone’s situation like progress percentage toward your goal or simple facts like whether you reached your saving targets or not. Info like that keeps you accountable on your journey without the unintended side effects.

Keep Yourself Educated About Financial Realities – Very few FIRE bloggers are trained financial experts, and that’s fine! Sharing real world examples of the FIRE journey is absolutely inspiring to a great many folks. But if you opt to write a blog about a financial topic, you have the responsibility to stay in touch (or maybe get in touch in the first place) with the financial realities for most people, including those who might be very different from you socioeconomically. If you don’t know anyone who couldn’t come up with $400 out of savings in an emergency – an attribute that describes half of the country – or if you read those income figures above and thought, Really?!, that’s a big sign that you have some work to do to get grounded in what most people are up against. The more that you reflect that reality in your writing, the better your blog will be, and the better it will serve your readers.

Your Turn!

Obviously I have strong feelings, but I’d love to know yours! For non-bloggers, what do you wish bloggers would universally do more or less of? Is there anything that would help you in your planning that bloggers aren’t generally doing now, or are doing and should stop? And for bloggers, what would you add to or subtract from this manifesto, and why? Anything you take issue with? Let’s discuss!

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!