If you’ve been reading more than a month or two, you know the question of when to retire has been on our minds big time for many months, ever since we realized that we’re significantly ahead of schedule on our saving plan. We’re talking about a relatively small time difference — sticking it out until year end, or leaving maybe in the summer or fall if we hit our numbers sooner — but opinions have been strong on both sides. There are those who’ve counseled us that we’ll never regret quitting as soon as humanly possible, and those who’ve urged us to collect those year-end bonuses and maybe save a little extra on the way there.

When we last talked about it here, we shared our then-current thinking: that we’d work until one of two things happen, either we hit year end or we reach our stretch taxable savings/investments goal. (Or option three: one or both of us get laid off. Not especially likely. More on this in a future post.)

But since then, some things have changed, and it’s led us to make peace with working until the end of the year. Today we’ll share why we made this mindset shift.

Before we dive into all of this, a few basic facts to ground all of this:

- We’ve revised our target “magic number” for our taxable funds to a stretch goal that is already about 20 percent higher than our original target number.

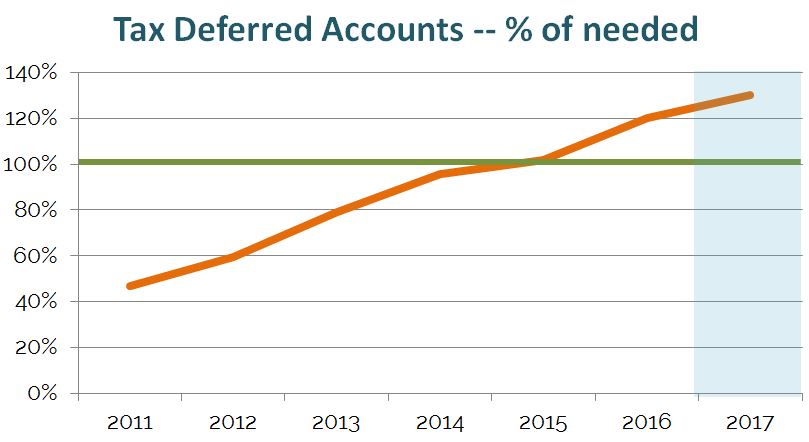

- Our 401(k)/tax-deferred funds, which we don’t plan to tap until age 60, are already significantly above what we project we’ll need to roughly double our monthly spending when Mr. ONL turns 60, assuming modest rates of return below historical averages. (Baller later years, here we come! Or, you know, maybe we’ll just be able to cover our health expenses.)

- We recently paid off the mortgage on our home, so we can save like gangbusters this year.

I say all of that to answer questions in advance about whether we’re being hasty in quitting at X time, or whether we’d be able to build up a nice cushion by working until the end of the year. Of course we can save more, but we don’t really need it.

Health Care Uncertainty

The single biggest reason I want to keep working through year’s end is the gaping health care abyss that we’re staring into. We care tons about having good health care coverage in early retirement, when we’ll no longer have access to employer-sponsored insurance, because we absolutely don’t want to end up like the quarter of Americans who struggle to pay their medical bills — even with insurance! — or the share of them who end up bankrupt.

While we still don’t know much about what the current presidential administration will mean for retirees — though there are still outstanding pledges to roll back Medicare benefits, among other things that affect traditional retirees — the biggest concern for anyone contemplating early retirement in America should be the lack of consensus around a replacement for Obamacare.

Our hope has been that Congress won’t repeal the Affordable Care Act until they have a reasonable option in place to replace it, and so far they seem to be sticking to that plan, given that they’ve had weeks now to repeal the ACA officially and they haven’t done so. And public pressure on them to keep affordable coverage intact is only increasing. That’s the good news.

The bad news is that the lack of action means none of us know what to plan or budget for, and worse, the delay may soon throw the current health insurance exchanges into chaos, and insurance companies may be forced to leave the exchanges simply because they lack clarity about what the new law might look like. This will mean that millions could lose coverage even with Obamacare and its subsidies in place. Enrollment was already down this year because of the country’s confusion around the ACA.

One good reason why we want continuous health coverage: that fall would be expensive.

We’ll keep monitoring the health care situation because we are intensely focused on this, and we’ll share more here as we know it, but in the meantime, we are seriously considering budgeting for a full rack rate health insurance plan not on the exchange, just to be on the safe side. And that’s a far cry (and many, many dollars — at least $10,000 per year) away from what we had been planning for.

It’s entirely possible that we won’t have answers by year’s end, but that’s still almost 11 months away, which we’re hoping is enough time to get a better idea of what’s coming next than we have now.

The Philanthropic Fund

As we urged everyone who could possibly afford it to do, we gave a lot to causes we care about at the end of last year. (Our nudging on it also earned us a brief Buzzfeed mention.) I don’t say that to brag, but to share that it was a galvanizing moment for us. We gave significantly more than we have in the past, because it’s such an important time to do so, and because we could. And we realized: we will be extremely sad if we can’t keep giving in retirement. We don’t expect to be able to give at the same levels, and of course we’ll make an impact by volunteering our time in abundance, but we always want to be able to give actual money, which is what most charitable causes need.

So we decided: everything we earn above our stretch magic number is money we can put into a donor advised fund, which will let us take the tax write-off in our last high tax bracket (and probably last itemizing) year, and will provide funds for future giving even when we can’t technically afford to give much. Knowing that any months after we hit the big number are going to fund our future giving will make them feel a lot more worthwhile than if we were just hoarding more for ourselves than we need.

The “Year of No” Is Working

We recently declared 2017 our “Year of No,” mostly referring to our new focus on setting boundaries at work. And here’s the crazy thing: It’s working.

In my case, I talked to my management about working smarter, not harder and getting more support to do so, and they came through for me. And I’ve talked with them about delegating more so that I’m creating opportunities for others while reducing my own workload, and they were supportive of that too. (Can I just say one more time how grateful I am to work for a wonderful company? My desire to leave is not about that at all.)

So far this year, I’ve been working weekly hours in the 40s, not the 60s, and have been able to empower others in the way I’ve always wanted to in order to leave behind a strong legacy of great people. If it continues this way, I will have no trouble making it through the end of the year.

More Money Is on the Table

In Mr. ONL’s case, some circumstances have changed that make it even more advantageous than in the past to stick it out til the end of year. And whether that extra money ultimately goes into our investments or our donor advised fund, it’s just one more argument in favor of sticking to our original (but already shortened) timeline.

Those Crazy Markets

We are staunchly opposed to meandering into talk of when the crash will come, and we no longer pay any attention to daily or weekly market fluctuations. But we’re overdue for a recession as is, and now the country is moving in an isolationist direction, which most economists believe is generally bad for countries’ economies. While we are absolutely not rooting for a crash, having it happen while we’re still working would sure be a lot easier to cope with than if it happens after we pull the plug. Plus, saving just a smidge more in anticipation of a big or extended correction wouldn’t be the worst contingency plan ever.

– – – – –

Is This “One More Year” Syndrome?

In a word, or actually two: Hell no. We’re sticking to our guns on this one, and quitting at the end of this year, no matter what, even if health care is unclear, and even if markets go all bajiggity. That’s been our plan all along, and is in fact still a lot sooner than our original goal of quitting in 2020. All we’re doing now is walking back the idea that we could even shave a few more months off of our timeline.

What Would You Do?

If you were in our shoes, would you stick it out til the end of the year, or pull the plug as soon as you possibly could? Are any of the factors that we’re thinking about on your mind as well? How are you planning (or not planning) for the health care uncertainty? Anybody else eyeing beefing up a donor advised fund? Let’s chat about it all in the comments!

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!