Year after year, research consistently shows that health care is one of the top worries for most Americans, and that’s no less true for early retirees. Practically every week I hear from would-be early retirees who say that they long ago hit their financial independence number, but can’t/won’t retire because they’re too anxious about health insurance availability and health care costs.

Which I totally get.

We’ve lived in a state of health care limbo for a while now, which I sometimes calls the health care abyss. Regardless of your politics, you have to acknowledge that the Affordable Care Act (ACA, aka Obamacare) has been a gift to early retirees, many of whom would otherwise not have any way to get health insurance outside of employment. But with the ACA being so politicized, we also all know that it could go away any time – or, more likely, parts of it would go away – and that can be stressful, especially for those with chronic health conditions. (Hi.)

But while none of us can see the future, and we don’t know what our options may be five or ten years from now, we can be smart about how we choose coverage for next year, or – for those who are currently planning for early retirement – how we use next year’s costs to project for the future.

It’s currently open enrollment season – and open enrollment closes in most states on December 15 – so if you need health care for next year, now is the time to do your homework.

But first…

I’m so excited to share a HUGE update on my upcoming book, Work Optional: Retire Early the Non-Penny-Pinching Way. The publication date has moved up six weeks to February 12! That’s less than three months away. If you’d like to read it, click over here to get more info on how you can pre-order it in hard copy or as an ebook, or how you can request your library purchase it. It will also be for sale as an Audible ebook (with my voice!), and I’ll let you know when that version is available. Thanks so much to everyone who has already ordered it! xoxo

Some Degree of Certainty for Now

Every time I write about health care, it seems to require repeating the caveat that this is not a political post. So this is that caveat. And this is the only thing I’ll say that has the least bit to do with politics: with last week’s election behind us, and Congress now split between the two parties for the next two years, we have some assurance that legislative gridlock will prevent any major changes to the ACA for at least the next Congress. The executive branch still has the ability to make administrative changes, and with the individual mandate in the law repealed already, it’s possible that exchanges could destabilize if many fewer people buy exchange plans in 2019 and beyond.

But barring any major catastrophes, early retirees with no employment-based insurance available should expect to be able to buy health insurance on an exchange through at least 2021. (The next Congress after this one won’t be seated until January 2021, and if they made changes to the law right away, the earliest they could take effect is the start of 2022.) Three states – Idaho, Nebraska and Utah – also just voted to expand Medicaid (a useful proxy for health care access that I detailed in this post), and three more are likely to follow suit with the governors’ seats flipping, which should further stabilize things.

This is the most certainty early retirees have had around health insurance in a while – possibly ever. But it’s still only short-term certainty.

Your Most Important Number: Out-of-Pocket Max

A surprising bit of good news for 2019 is that the premium costs of most health insurance plans on the exchanges are stabilizing, a welcome trend considering that exchange plans have been increasing in price the last few years by many multiples of inflation in the bulk of states. In 11 states, exchange plan premiums have actually gone down for 2019, but overall, premiums are up about three and a half percent, much closer to inflation itself, and fairly reflective of the four percent increase projected for employer-based health care costs for 2019. Some experts believe insurance costs overall are now stabilizing in the ACA era as insurance companies have returned to profitability, so we’ll all keep fingers crossed that this trend holds for 2020 and beyond.

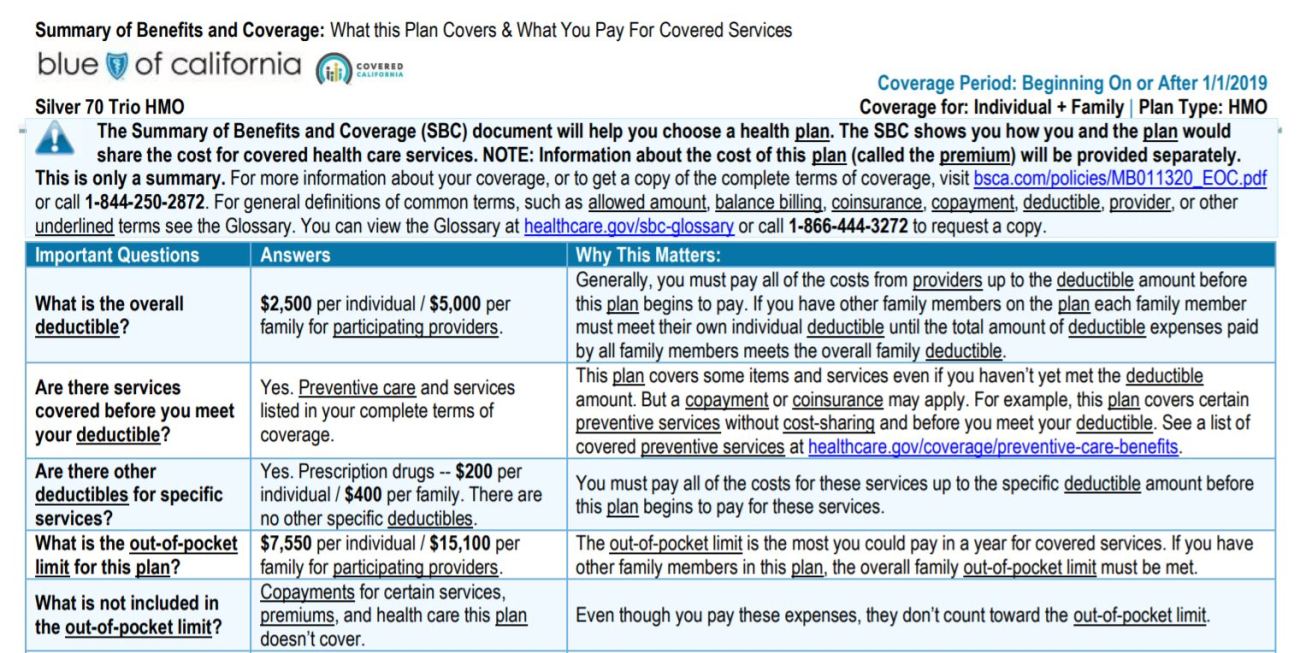

However, all of that said, the cost of premiums is only one part of the equation, and it’s not the most important number for you to keep in mind when looking at potential health care costs. The premium is the amount you know for sure you’ll have to pay out every year, but the number you should care most about is your out-of-pocket maximum, in essence your worst case scenario.

The out-of-pocket maximum is often not listed on the summary view of available plans when you search on the exchanges, and you may have to click on a plan and scroll down:

FYI, for all examples in this post, I’ve used an early 40s couple with $50,000 per year in MAGI (gross income minus qualified retirement savings contributions, essentially), living in Los Angeles County.

Every plan by law must use a uniform summary of benefits form to make clear to you all of your costs – it’s great for comparing plans to one another! – and this form must tell you what the out-of-pocket max is and what’s included in it or not:

Most out-of-pocket max descriptions will look like this one: clarifying that “out-of-pocket” does not include plan premiums or copays/coinsurance on services you pay for before you hit the maximum. So your total cost could be quite a bit higher than the max shown, but you can add the cost of your premiums and a few thousand dollars buffer to estimate what your true max could potentially be.

I’ve written in detail about estimating your costs for exchange plans and comparing them to one another, so please consult that post if you’re looking at health insurance plans on the exchange for the first time.

All Deductibles Are Not Created Equal

As I’ve done more research, I’ve concluded that high-deductible health plans (HDHPs) and their accompanying health savings accounts are not the money-saving miracle that they are often made out to be by those who tout their tax-avoidance benefits – namely because most people won’t actually come out ahead financially on a high-deductible plan, and because high deductibles create massive disincentives to receiving care, even for those who can afford it regardless – but here’s one more argument against HDHPs:

All deductibles do not work the same way.

Related post: The Problem with the HSA (Health Savings Account) Isn’t the HSA

Even if a non-HDHP plan cites a deductible of some amount, that doesn’t actually mean that the deductible applies to every expense. In the Blue Shield California example for the LA County couple, the standard silver plan shows a deductible of $5000 for the family, but if you look more closely, you see that quite a few services don’t require the deductible to be met before paying, including all emergency and urgent care services aside from ambulances:

The HDHP bronze plan offered to the same couple, however, has the deductible applying to absolutely everything except for the free preventive care visit required by law:

So it’s important to look not just at deductible amounts, but actually to look at service costs in detail to see where the deductible actually applies, and where it doesn’t. Our current health care plan has a relatively high deductible, but despite going to the emergency room and getting several expensive tests and imaging procedures done this year, I haven’t actually had to dip into my half of the deductible at all, because it didn’t apply to any of the care I’ve received.

Do your homework not just on deductible amounts, but on what they apply to and what they don’t.

Be Mindful of Your Own Circumstances

As I shared when talking about choosing this year’s health insurance, we ended up selecting a different plan than the one we originally expected to buy based on vastly unequal prescription drug coverage. That was important in our case, and so it’s the factor that won out. And in a plot twist, we just received a letter from our insurer that they’ll no longer be covering non-emergency care outside of California, a highly problematic development for those living near the state line whose closest city (and therefore entire health care team) is next door in Nevada. So we’ll be switching back to our originally intended plan for 2019 and figuring out how to bring drug costs down in other ways. (This is why it’s so important to review the plans closely every single year.)

What’s important for you isn’t necessarily either of these factors, but to know your own situation and needs. If you’re nowhere near a state border and don’t require autoimmune drugs, then you can focus on provider network as most important, something you can research right from the plan page on the exchange. Or perhaps you care most about benefits like how many physical therapy or acupuncture visits the plan covers. Know what you need, and research what your plan options offer.

Project for the Future, Including Traditional Retirement

For those still saving, the best thing you can do for your future finances and current peace of mind is to estimate what your health care would look like for 2019 if you were buying it on the exchange, and then do two things:

Factor next year’s expenses into your future retirement budget along with an increase factor greater than inflation (we estimate 8-10% a year), and

Factor next year’s out-of-pocket maximum into your plans to ensure that you could afford to pay it, in addition to premiums, in any given year and still be okay financially.

One of my biggest arguments against aiming for the smallest possible early retirement budget is that it doesn’t allow enough wiggle room to accommodate potential health care realities. If you’re only budgeting for health care premiums, that’s not enough.

And as of now, the average out-of-pocket costs for Medicare recipients, above and beyond premiums paid, are nearing $300,000 between age 65 and the end of life. That works out to well more than $10,000 a year, with much of that skewed toward the last few years of life. If you’re aiming toward a “spend it all down to zero” vision of traditional retirement – something I don’t believe is actually common among early retirement aspirants – I urge you to reconsider.

Weighing All the Risks

I know it can feel discouraging to look at these large costs for health care. I know it’s tempting to consider options that aren’t real insurance like health care sharing ministries. I know it can even be tempting for those with ongoing health challenges to decide never to quit working. But what each of us ultimately needs to do is weigh all the risks, not just the most obvious ones.

With my ticking genetic clock, I had the reminder that I couldn’t necessarily wait until traditional retirement age to do all the things I want to do in life. And I truly feel lucky for having that reminder, because none of us are promised any amount of time, and if I hadn’t had that nudge, I might still be blindly continuing through life, never questioning if another path was possible, and taking my young, healthy years for granted. Instead, I appreciate them so much more.

For me, the equal and opposite risks were obvious: risk running out of money in early or traditional retirement, or risk spending all my good years working.

It’s up to you to take an honest assessment of what your risks are, because only then can you truly decide what’s worth the risk and what’s not.

Your Turn

Chime in with your thoughts and questions! Any questions you have about health care that you haven’t been able to get answered anywhere else? Any hints or tips you’d like to share with others here? Any decisions you’ve struggled with that you can share for others’ benefit? Let’s chat in the comments!

Don't miss a thing! Sign up for the eNewsletter.

Subscribe to get extra content 3 or 4 times a year, with tons of behind-the-scenes info that never appears on the blog.

Wohoo! You're officially one of our favorite people. ;-) Now go check your email and confirm your subscription so you don't miss out!